Contact us today!

How Appreciation of the Chinese Yuan will Effect Minor Metal Prices: Part I

Part I: Why China Will Allow Greater Appreciation of the Yuan

Part I: Why China Will Allow Greater Appreciation of the Yuan

Part II: What Appreciation of the Yuan Means for Minor Metal Prices

–

“China will continue to steadily advance the reform of the formation of the renminbi exchange rate mechanism under the principle of independent decision-making, controllability and gradual progress,” Chinese President Hu Jintao.

–

Following China’s decision to allow its currency, the yuan, to appreciate by a token half a percent against the US dollar last month, analysts have continued to speculate what the next exchange rate move by China’s government will be and when it may come. In the first of this two-part series, we talk economics. First we discuss exchange rate regimes and the domestic economic problems arising from China’s current exchange rate policy. We then explain why the only effective resolution to China’s economic issues is to allow greater appreciation of the yuan. In Part-Two, we will discuss how appreciation of the yuan will impact the international prices for a number of minor metals.

Exchange Rate Regimes & the Renminbi – the Fundamentals

Most western economies allow their currencies to float freely against each other. Currency trading by international banks and investment institutions accounts for the majority of global currency transactions and relative values are determined by the corresponding global demand for each currency. Demand for currencies is primarily based on national economic and trade data (employment rates, productivity analyses, import/exports statistics etc.). One of the strongest arguments in support of freely floating exchange rates is that they provide the international economy with a natural response mechanism to deal with trade imbalances. As one national economy strengthens against another, currency traders, speculators and investors invariably move to invest in that country through various methods. The consequent demand for that country’s currency leads to an appreciation against other currencies, thereby making weaker economies’ exports more affordable and the stronger economy’s exports less relatively more expensive.

In contrast, fixed exchange rate regimes, which the yuan (also referred to as the renminbi or RMB) can be considered a de facto member of, can be very effective for developing countries by ensuring more stable prices for their export markets; A significant boon to economies – like China – that are heavily dependent upon international trade. However, these benefits come at two large expenses: (1) the loss of ability to use independent monetary policies (interest rates) as a method to control the domestic economy, and (2), vulnerability to ‘imported inflation’. Countries that fix their exchange rate lose the ability to use their central bank’s interest rate to influence the economy because the money supply is determined by the central bank’s target exchange rate. The central bank, therefore, must increase (or decrease) the money supply at a rate equal to the rate of the foreign currency to which it is pegged. Through a process called sterilization, all the foreign investments by a central bank in a fixed-rate economy made to control its domestic currency from appreciating (such as US Treasury Bond purchases) must result in the injection of an equal amount of cash into its own economy. As a result, such countries do not only lose the interest rate as a mechanism to influence economic growth and control inflation, but also become susceptible to destabilizing expansionary monetary policy originating in the foreign country, a phenomenon known as ‘imported inflation’.

Repercussions of China’s Exchange Rate Policy

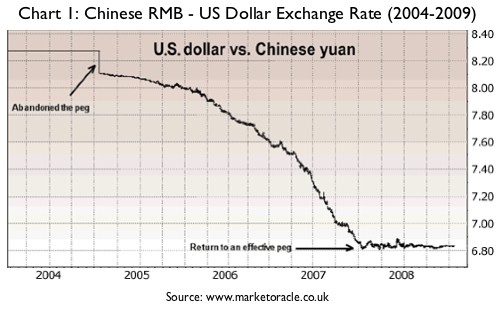

Economic observers are well aware that China has been actively involved in currency markets for a number of years through the purchase of significant quantities of US Treasury Bills. Chinese purchases of US Treasuries have become more pronounced since mid-2008 when the Chinese government decided to effectively peg the renminbi to the dollar the US dollar at a rate of Y6.8 to $1. This followed a brief experiment between 2005 and 2008 when China allowed the yuan to float somewhat freely, which resulted in its appreciation of 21 percent against the dollar. By 2010, Chinese purchases of US Treasury Bills averaged US$ 1 billion per day.

China’s involvement in – dare we say manipulation of – the currency market is not without serious repercussions. And it is the domestic economic repercussions of their actions that are the key to understanding the pressures on China’s policy makers.

First, let’s look at an example of imported inflation, where country A, which we will refer to as ‘China’, pegs its currency to country B, which we will call ‘America’. Assuming America is practicing an expansionary monetary policy, by lowering interest rates and increasing the money supply in order to stimulate the economy, By consequence, in order to keep its currency from appreciating, China must also increase its money supply at an equal rate. This is not a problem if both economies require the same monetary policies to maintain economic stability. However, once this correlation breaks down, problems begin to occur. For example, if China’s economy were growing at a faster rate than America’s and required high interest rates to stifle growing inflation, whereas America’s economy was suffering from high unemployment and low economic growth, and required monetary stimulus (low interest rates), such a situation would likely result in ‘imported inflation’. That is, inflation triggered not by domestic monetary policies, but by monetary policies of the foreign country due to its currency peg. By maintaining its currency peg, China must follow the same monetary policy as America – an expansionary policy – at a time when it should be increasing interest rates and pursuing deflationary policies. This essentially describes the monetary relationship between the Chinese renminbi and the US dollar since early 2009 when the Chinese economy quickly rebounded from the global recession while the US economy struggled.

A second factor influencing China’s domestic economy is the influx of cash provided by China’s massive economic stimulus package announced in the wake of the 2008 economic downturn. The stimulus package resulted in greater domestic spending and investment, which, in turn, increased demand for RMB. In a fixed exchange rate economy, an increase in demand provided by fiscal stimulus is generally offset by a consequent rise in prices and wages. Recent strikes in Guangdong by workers demanding higher wages as well as the upsurge in China’s energy costs and housing prices over the past two years are evidence that the Chinese economy is experiencing textbook price and wage adjustments (increases). As the economy digests the fiscal stimulus package, the only long-term effect will be inflation.

The current economic situation in China is a result of the two factors noted; A monetary policy that has placed greater importance on exchange rate stability than inflation and a fiscal policy that has pumped billions of RMB into the system over the past two years. As shown, both factors directly result in higher inflation. It is no wonder why China’s inflation rate has rebounded quickly this year, forcing the government to revise its annual inflation expectations before the mid-point of the 2010.

The Solution

Over the past six to twelve months, the Chinese government has implemented a series of band-aid policies targeting the industries most heavily impacted by inflation, including restrictions on second-home purchases and increasing reserve requirements of domestic banks. Raising bank reserve requirements (thereby limiting how banks can lend out and how much cash is in the system) has had a broader effect in cooling the domestic economy than most other policies, but the application of this method is also limited as it threatens to make banks unprofitable, which would result in even more economic instability. As the Chinese government and People’s Bank of China are well aware, the most effective and direct method to address the domestic inflation problem would be to allow an appreciation of the RMB. Simply put, this would allow the central bank to slow down its printing presses and decrease the speed of money supply growth.

Given the need for China to relieve inflationary pressures and the threat of increasing American trade protectionism, we strongly believe that there will be a significant exchange rate policy change in the second half of 2010. How significant the policy change will be is difficult to say. However, given China’s proclivity to incremental policy changes and concerns about sudden, potentially destabilizing effects, it is likely that any change will occur within the controlled (or managed) float system that was used prior to 2008 and has been used in name only since. What is certain is that there will not be a one-off revaluation of 10 to 20 percent, which some analysts have suggested, nor will there be any consideration given towards adopting a freely floating exchange rate. SMI Ltd. expects an actual appreciation of the yuan against the dollar of between five to ten percent over the next 12 months.

Comments

0